The Moneyball Series: What Really Drives Startup Success? Episode 2: How Important is Accurate Market Sizing?

Top down vs bottoms up and whether market sizing exercises matter

Let's get this out of the way first: market size matters.

Why? As it pertains to VC investing, VCs need to know whether or not there is enough money to be made in a particular market for them to take the outsized risk of investing in a brand-new company with nary a customer or, in some cases, a product. Funds are beholden to their LPs, who expect certain rates of return. And knowing that most investments don't pan out, VCs count on a few deals generating 10, 20, 50 or even 100x to make up for the low performers. Not every deal will generate 10-100x returns, of course, but every deal must have the potential to be a unicorn in order for the math to work– which is why, again, market size matters.

But how important is it for founders and VCs to get those numbers right at the outset? How crucial is it for the TAM, SOM, and SAM to accurately reflect the opportunity? After all, startups pivot and expand their product range all the time, and with every pivot, these numbers can change quite significantly. Funny story–I once worked for a YC-backed startup that started out as a dating app and eventually pivoted to HR software. As you can imagine, any market sizing exercises that the founding team did ended up being wildly off.

Markets are also created and destroyed, seemingly overnight. Just five years ago, global AI spend was hovering around $50Bn. Today, it's estimated to be $190Bn. By 2027, it's projected to reach $500Bn. On the flip side, the NFT market has expanded and contracted, almost in the same year.

To get to the bottom of this question, let's take a look at some of the most famous tech companies for answers. Surely the VCs who backed these companies conducted extensive market sizing exercises to determine that they were, in fact, venture-backable. In this exercise, we'll take compare the companies' market-size estimations in their initial pitch deck to what they actually are today.

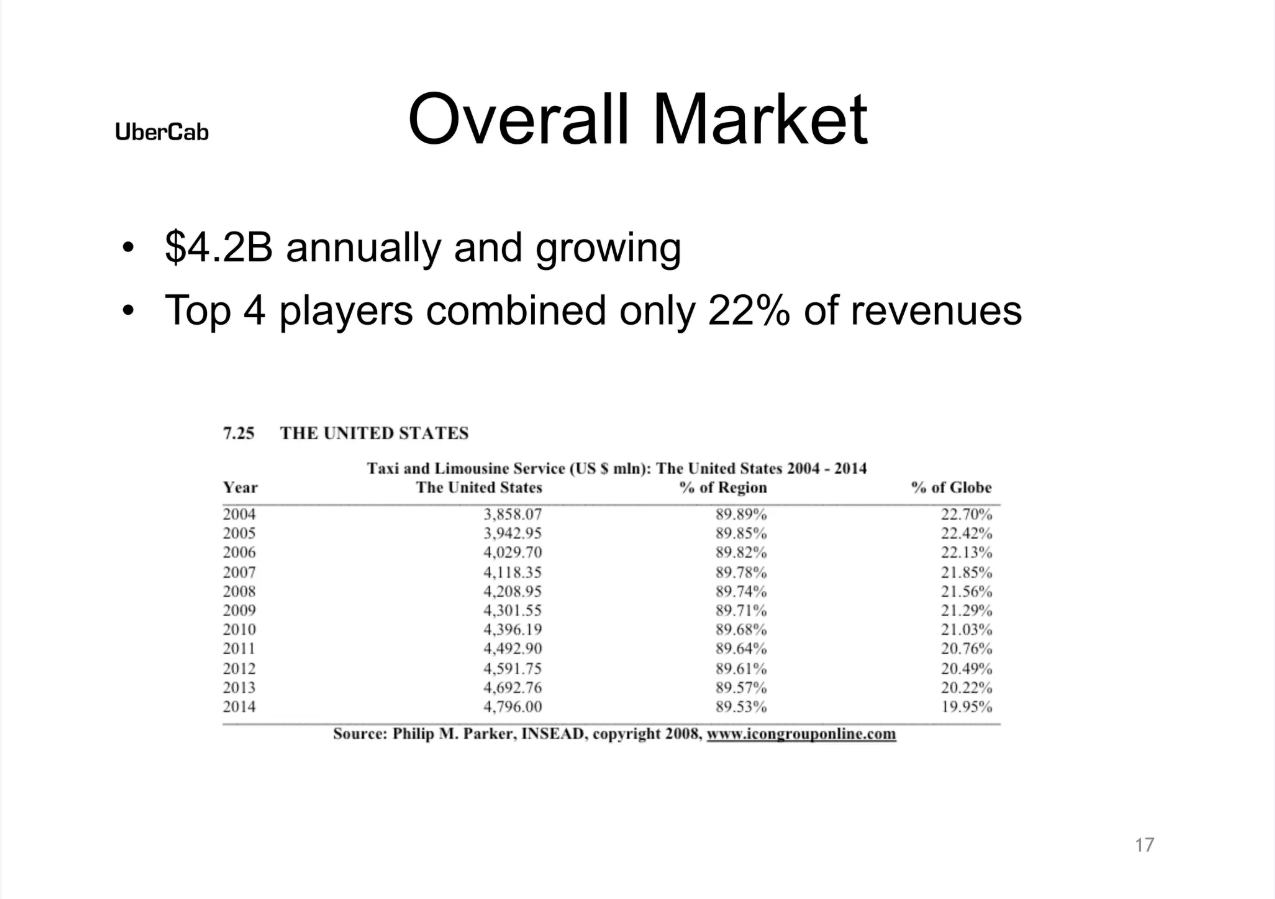

Uber

When Uber first came onto the scene, it aimed to replace taxis and limousine services in major U.S. metropolitan areas like New York and San Francisco. It owned a small fleet of luxury cars deployed in San Francisco, mostly to shepherd Bay Area executives to and from their offices and the airport.

The company understood its potential, though, and predicted that it would soon penetrate other major U.S. markets. But even under its most generous projections, Uber couldn't foresee that the U.S. ride-hailing market would be $54.7Bn in 2025, growing at a 2.7% CAGR, and $175.7Bn worldwide at a 4.9% CAGR. Not only did the company effectively replace taxi and limo services in many areas, but it also expanded its service offering to include food delivery, freight and logistics, micro-mobility, and even financial services.

Airbnb

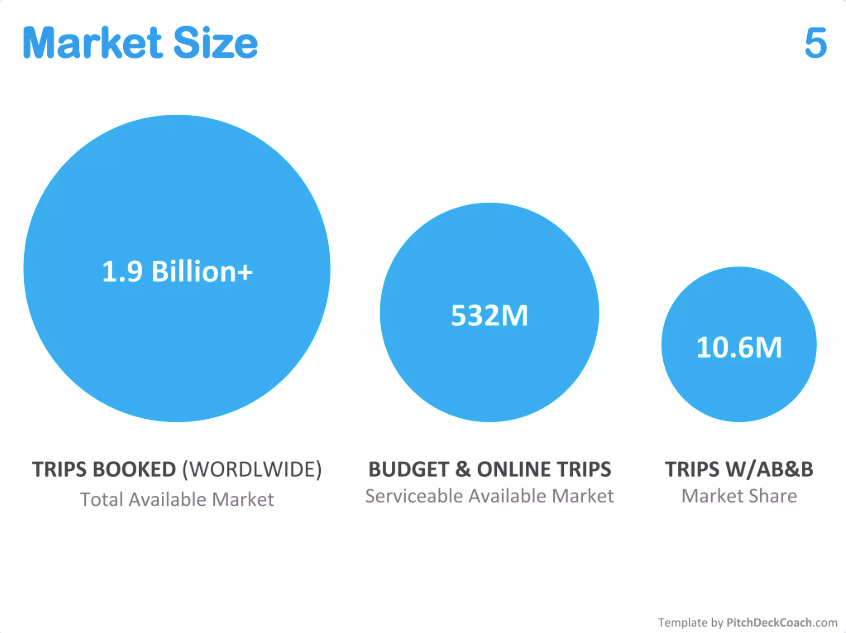

Airbnb is a personal favorite of mine. Not only am I (still) an avid Airbnb'er, I love that its founders didn't attend a top university. It's hard to glean from its pitch deck alone, but it seems that Airbnb's TAM is the total number of trips (vacation or otherwise) booked worldwide. It thought it they would be competitive in the budget and online trips category, where it would charge a transaction fee (average $20), which would put its TAM at $38Bn and their SAM at $10.6Bn. It thought it could capture 2% of that market, bringing its SOM to $212M.

How very modest of Airbnb. Today, the global vacation rental market is $89.3Bn at 3.7% CAGR and the company's annual revenue hovers around $11.1Bn.

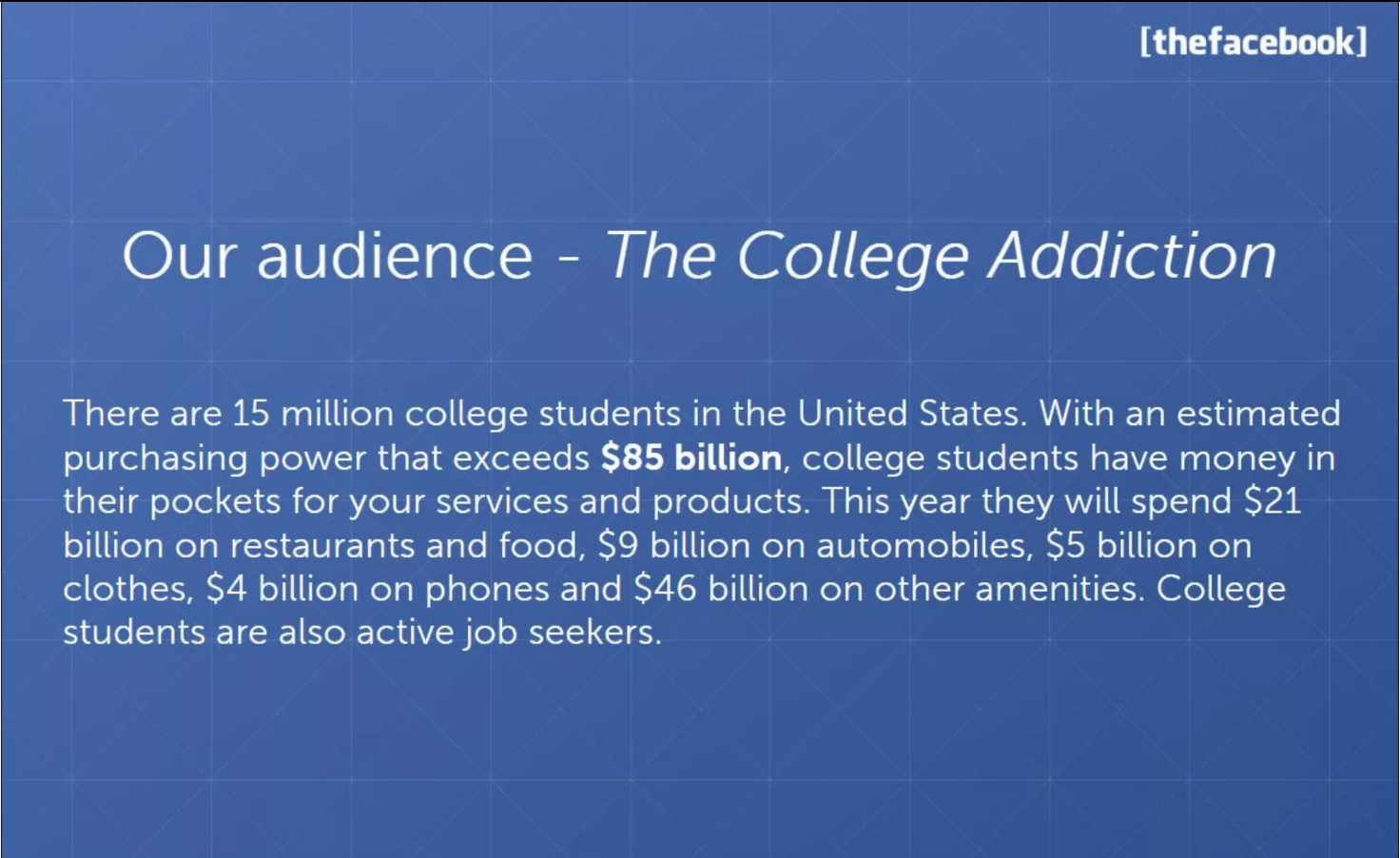

Facebook famously started out as a social media site for college students and, in its early days, was exclusive to Ivy League students. Recognizing its growth potential, the startup quickly expanded to college campuses across the country. Friending people on Facebook became the way students got connected, and the story of the company's eventual rise has become the subject of countless think-pieces and Hollywood movies. No one could have predicted the market Facebook would create, least of all Facebook itself. The company thought that if it could capture even a portion of the spending power of U.S. college students–estimated at $85Bn in 2005– it would be golden.

I don't need to tell you what the social media market is today for you to know that it is massive. Global spending on social media advertising alone is projected to reach $277Bn this year. Facebook has long since grown from its roots and is now one of the largest companies in the world.

Conclusion

To be fair to all of the companies above, they are outliers, and ambitious as their founders may have been, they couldn't have guessed the markets they would go on to create and the spaces they would eventually occupy.

This exercise is simply meant to demonstrate that while market size matters and is an essential component to a good pitch deck (although there are a number of very famous companies that didn't even bother with market-size slides), getting the numbers exactly right is not necessary.

Founders and VCs should be encouraged by this. As long as the market that the startup operates in is big enough to potentially provide 10x returns, it is a VC-backable business.

One caveat: terrible, wildly inaccurate, or illogical market size estimations highlight the founding team’s inability to understand the market in which they operate, which is a red flag. It shows a startup that lacks a solid go-to-market strategy and is ignorant about their competition. In the worst case, it suggests a market that doesn’t exist—meaning VC investment isn’t going to happen. So while it’s not important to get everything right from the outset, it is important to be able to defend your numbers as a sign of competence.